UCO Bank is a government-owned bank operating in the Indian banking and financial services sector. With improving asset quality, credit growth, and government support, the bank is gradually strengthening its fundamentals.

Investors are actively searching for UCO Bank Share Price Target 2025, 2026, 2030, 2035, 2040, 2045, 2050 to understand its long-term potential. This article provides a structured, data-driven analysis of UCO Bank’s growth outlook.

Company Overview

UCO Bank is a public sector bank that provides services like retail banking, corporate banking, loans, deposits, and digital banking solutions.

The Indian banking sector is expected to grow steadily due to:

- Rising credit demand in retail and MSME sectors

- Government push for financial inclusion

- Digital banking expansion

- Economic growth and infrastructure development

These factors create a positive long-term environment for banks like UCO Bank.

Current Share Price

Financial Overview Table

| Metric | Value |

|---|---|

| Market Cap | ₹33,293 Cr |

| P/E Ratio (TTM) | 13.48 |

| P/B Ratio | 1.20 |

| ROE | 8.87% |

| EPS (TTM) | ₹1.97 |

| Dividend Yield | 1.47% |

| Industry P/E | 13.23 |

| Book Value | ₹22.20 |

| Face Value | ₹10 |

Interpretation:

- Valuation is reasonable and close to industry average

- ROE is improving but still moderate

- Dividend yield adds some income stability

- P/B near 1.2 suggests limited overvaluation

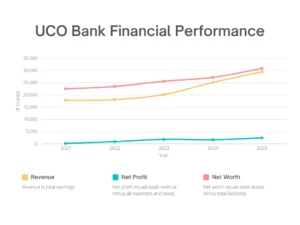

Financial Table

| Year | Revenue (₹ Cr) | Profit (₹ Cr) | Net Worth (₹ Cr) |

|---|---|---|---|

| 2021 | 17,870 | 167 | 22,516 |

| 2022 | 18,082 | 895 | 23,469 |

| 2023 | 20,159 | 1,826 | 25,604 |

| 2024 | 25,120 | 1,654 | 27,214 |

| 2025 | 29,474 | 2,445 | 30,885 |

Profits and Revenue Analysis

UCO Bank has shown strong improvement in both revenue and profitability over the last five years.

- Revenue increased from ₹17,870 Cr in 2021 to ₹29,474 Cr in 2025

- Profit increased significantly from ₹167 Cr in 2021 to ₹2,445 Cr in 2025

This indicates:

- Strong turnaround from weak profitability phase

- Better asset quality and reduced NPAs

- Improved operational efficiency

The bank is clearly in a recovery and growth phase, which is a positive sign for investors.

UCO Bank Share Price Target 2025

The UCO Bank Share Price Target 2025 was estimated in the range of ₹28.5 to ₹30.5, reflecting performance in the public sector banking segment.

UCO Bank operates in retail banking, corporate lending, and digital financial services, benefiting from improving credit demand and banking activity. The bank maintained stable financial performance supported by better asset quality and reduced non-performing assets. Its focus on loan growth and digital banking expansion contributed to operational stability. However, factors such as interest rate fluctuations and regulatory policies influenced short-term price movement. Overall, the UCO Bank Share Price Target 2025 indicated moderate growth driven by banking sector recovery.

UCO Bank Share Price Target 2026

By 2026, the bank is expected to continue its recovery and stabilize profitability.

Target Price (2026): ₹30.5 – ₹45

Rationale:

- Continued improvement in profits

- Stable credit growth

- Better asset quality

UCO Bank Share Price Target 2030

By 2030, the banking sector is likely to expand significantly with economic growth.

Target Price (2030): ₹70 – ₹90

Rationale:

- Higher loan growth

- Improved efficiency

- Better return ratios

UCO Bank Share Price Target 2035

Long-term structural improvements may reflect in stronger valuations.

Target Price (2035): ₹110 – ₹140

Rationale:

- Stronger balance sheet

- Consistent profitability

- Increased investor confidence

UCO Bank Share Price Target 2040

By 2040, the bank could become more competitive with private players if execution improves.

Target Price (2040): ₹160 – ₹200

Rationale:

- Digital transformation

- Higher margins

- Stable long-term growth

UCO Bank Share Price Target 2045

The bank may achieve maturity with steady earnings growth.

Target Price (2045): ₹220 – ₹280

Rationale:

- Consistent business expansion

- Stronger fundamentals

- Stable returns

UCO Bank Share Price Target 2050

In the long term, the bank’s performance will depend on structural reforms and execution.

Target Price (2050): ₹300 – ₹400

Rationale:

- Long-term economic growth

- Banking sector expansion

- Improved efficiency and scale

Shareholding Pattern Analysis

| Category | Holding (%) |

|---|---|

| Promoters | 90.95% |

| Retail & Others | 4.57% |

| Other Domestic Institutions | 4.12% |

| Mutual Funds | 0.28% |

| Foreign Institutions | 0.08% |

Analysis:

- Very high promoter holding reflects strong government control

- Low institutional participation shows limited market confidence so far

- Retail participation is small

This structure is typical for PSU banks but also limits aggressive re-rating unless institutional interest increases.

Factors Affecting Share Price

- Asset Quality Improvement

Reduction in NPAs is a key driver for profitability and valuation. - Credit Growth

Higher loan disbursement, especially in retail and MSME, boosts revenue. - Interest Rate Cycle

Changes in interest rates directly impact net interest margins. - Government Policies

PSU bank reforms and recapitalization play a major role. - Competition from Private Banks

Private sector banks with better efficiency can limit market share growth. - Digital Banking Adoption

Improved digital services can enhance customer base and efficiency.

Conclusion

UCO Bank is showing clear signs of recovery with strong profit growth and improving fundamentals. However, it still faces challenges like moderate ROE, high government ownership, and limited institutional interest.

The stock offers:

- Stability due to government backing

- Gradual growth potential

- Turnaround opportunity

But it is not a high-growth stock yet. Investors should keep expectations realistic and focus on long-term progress.

FAQs

- What is UCO Bank Share Price Target 2026?

The expected range is ₹45 to ₹55 based on current growth trends. - Is UCO Bank a good long-term investment?

It can be a moderate long-term option, especially as a turnaround PSU bank. - What are the main risks in UCO Bank stock?

Low ROE, high government control, and competition from private banks. - Does UCO Bank pay dividends?

Yes, it offers a dividend yield of around 1.47%. - Is UCO Bank undervalued?

It is fairly valued near industry averages, not deeply undervalued.

Disclaimer

The information provided in UCO Bank Share Price Target for 2025, 2026, 2030, 2035, 2040, 2045 and 2050 blog is for educational purposes only and does not constitute financial advice. Investors should research and consult with a financial advisor before making investment decisions.

Call to Action

Stay updated with the latest trends like UCO Bank Share Price Target 2025, 2026, 2030, 2035, 2040, 2045, 2050 and forecasts by visiting sharesprediction regularly. Our comprehensive analysis and insights can help you make informed investment decisions.